Being Digital is the Biggest Banking Opportunity Ever

25 Jun 2015

by Darren Oddie

Strategy Director, Wipro Digital

@DarrenOddie

Arguably, digitization of banking is the biggest disruptor in banking history. Some believe the impact will be bigger than the 1930’s depression and the recent financial crisis.

Whilst many banks are pursuing digital transformation programs and projects, progress is often thwarted by organizational culture and design. The tradition of working one’s way up through the banking ranks has ensured that career bankers fill bank boardrooms. These are people with a natural preference for financial engineering. Today’s digitally-enabled world, however, requires bank board members filled with a passion for surpassing ever-changing customer needs, more than finance savvy.

Digitization, properly implemented, is a powerful transformation agent for banks that want to remain relevant in a fast changing and increasingly competitive environment.

Bank Transformation: Opportunities & Challenges

It’s genuinely difficult to transform an incumbent bank and this list is not exhaustive or prioritized. Banks must:

â Rebuild broad stakeholder trust. (The recent financial crisis and government bail out of many banks has forced new moral and commercial agendas for banks to deliver on.)

â Build brand equity by bolstering capital efficiency - increase revenues, decrease costs and increase customer satisfaction.

â Satisfy regulators by delivering on new requirements to tighten internal controls, risk management and increase financial strength.

â React to global incumbents’ scale agendas – addressing customer churn caused by aggressive price competition.

â Fight the rise of digitally native (and thus efficient) neo-banks, Tech and/or FinTech.

â Deal with consumers ever-changing digital experience needs.

â Re-architect their businesses and technologies to be customer-centric, adaptable and agile. Automate processes and becoming truly data empowered.

â Change their banking culture.

To accelerate a digital transformation agenda, it’s worth considering how digitally native FinTech aggressors operate. Whilst a bank is far more complex than a startup, there are lessons that can be learned and acted upon.

Learning From FinTech

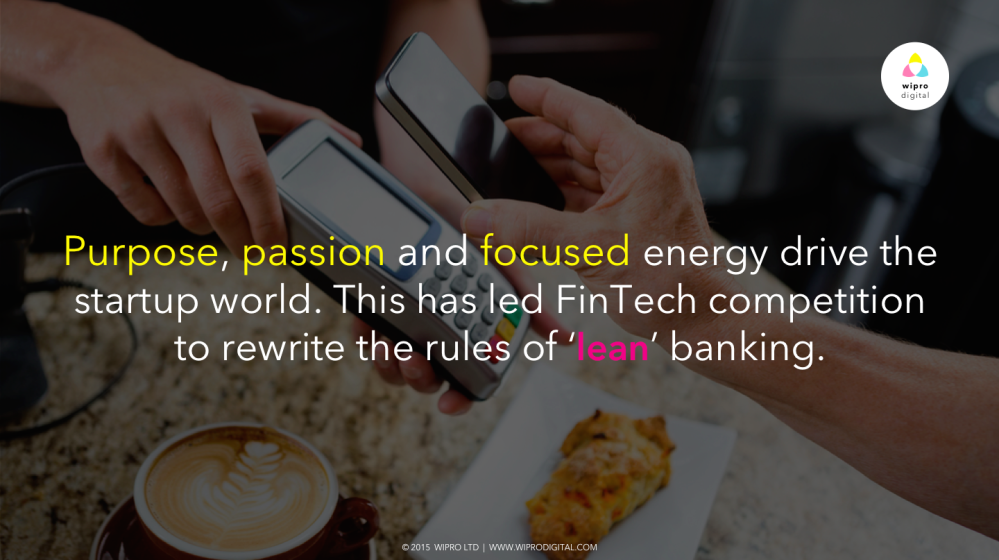

Purpose, passion and focused energy drive the startup world. This has led FinTech (and Tech) competition to rewrite the rules of ‘lean’ banking. From a customer perspective this transpires as low cost products that offer a great experience and engaging dialogue (keeping you, the customer, close to the brand). When a business is social and/or mobile first (such as M-Pesa, Fidor, eToro or WeChat) it’s in a much stronger position to win and better engage customers.

Players such as Simple, Lending Club, TransferWise, Wealthfront, and Venmo introduced digital, data driven services that offer great context-based user experiences. Rather than just offering financial products or services, they use their technology, data and design to better the customer’s financial experience.

Customers know they can enjoy low-cost financial services and great experiences, so many shop around for specific ‘banking’ needs. A primary account is held with the incumbent bank, a secondary account is managed via Simple, and lend (save) money is with Lending Club. Monies can be transfered abroad with TransferWise, invested with Wealthfront, and friends can be paid (say, for splitting a dinner bill or taxi), via Venmo.

The traditionally steady state world of banking is now a fast changing industry, where the best CEOs create a purpose, passion and focused energy on being digital.

Actionable Transformation

Being digital requires an actionable digital transformation agenda that puts customers at the forefront and center of all bank activity.

Customer first thinking means designing customer experiences based on customer needs, key ‘moments of truth’ and context. This is different to driving customer transactions led by organization, product, service, channel or technology. Cross-functional bank teams collaborate to pursue parallel tracks of delivering amazing customer experiences whilst bolstering capital efficiency, increasing revenues, and decreasing costs.

Customer Journey Engineering, as practiced by Wipro Digital, enables this.

“Digital transformation is more than a facelift to the frontend – it has to encompass and integrate all backend processes that impact customer experience, such as logistics, billing, production, customer service etc.”

Here are four requirements for digital transformation:

â Customer Centricity: Break down organizational silos by putting the customer first each and every time. Customer-centered innovation workshops comprised of empowered multi-disciplinary teams ideate customer experiences that are easy to understand and consume. The aim is a flawless experience across any channel, driven by the customer’s choices: banking that delivers at any time, any place and any speed. There’s no grand strategy or grand master plan to deliver on. Banks will be agile and adaptable.

â Adaptive Architecture: Architect an evolved environment that is loosely coupled or de-coupled from legacy systems and processes to enable engineering to deliver at speed and at scale. Self-sufficient and open components ensure easy adaptation for the next disruptor.

â Application of Automation & Simplification: Projects, as there are multiple opportunities and challenges to address deliver flawless customer experiences whilst eliminating costly processes that have superfluous human interventions. The aim is to orchestrate more delightful customer interactions, through direct and/or indirect channels. For the customer, all channels deliver personalized and timely banking services.

â Data Empowered Insight: Use clean and consistent customer based data empowered insight to drive all the above and deliver contextualized customer experiences. Use customer insights that matter.

Digital transformation (being digital) is difficult, yet possible. It’s the biggest banking opportunity (ever) to delight customers with amazing experiences whilst bolstering capital efficiency, increasing revenues, and decreasing costs.

Originally posted via Wipro Digital

1.png)

Please login to comment.

Comments